Don’t overcomplicate your personal finance: 10 Rules to help you build wealth

I have a confession:

For years, I thought I needed to become a financial expert to manage my money well.

I’d see articles about optimal asset allocation and tax-loss harvesting and think:

Yikes… I should probably understand this stuff before I make any financial decisions.

So I’d do nothing because it all felt too complicated and intimidating.

I often hear the same thing from women:

“If I don’t understand investing jargon, I probably shouldn’t bother.”

“If I’m not maxing out my retirement, I’ve already failed.”

“If I don’t know what a Roth conversion ladder is, I must be behind.”

But here’s what I’ve learned:

Most of the financial stuff that really matters is shockingly simple.

The Problem

We overcomplicate money.

We see terms like “diversified portfolio rebalancing” and immediately feel out of our depth.

So we procrastinate. We wait until we “understand it all.”

And meanwhile, the basics that actually build wealth go untouched.

The Big Small Thing

Personal finance can be shockingly simple.

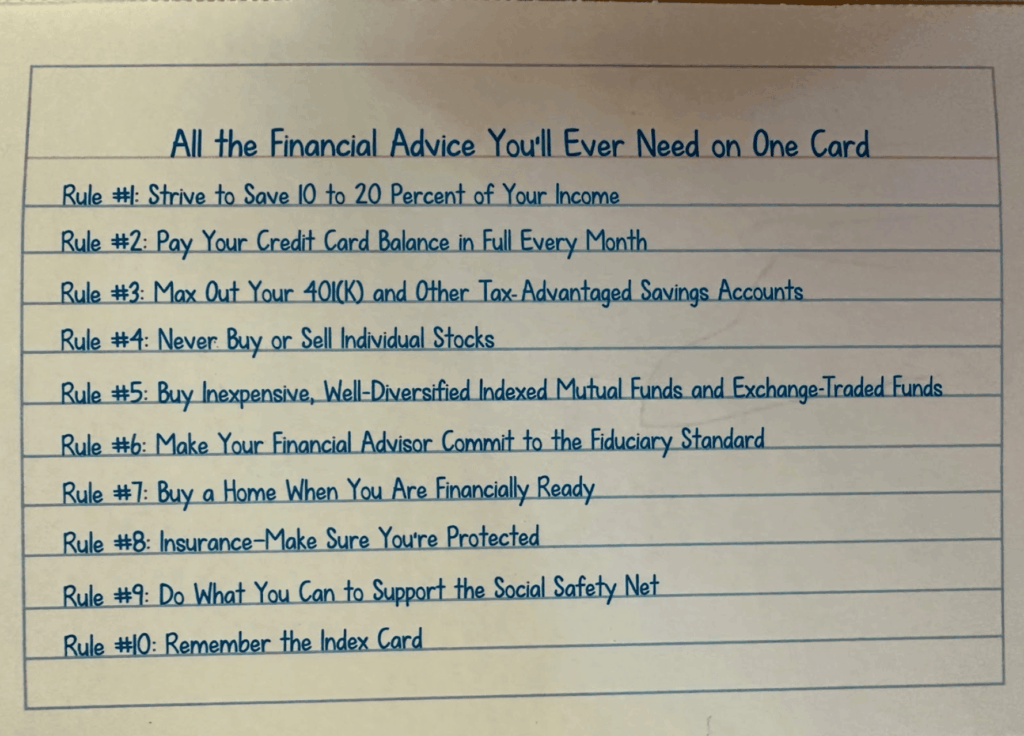

All the advice you need fits on one index card.

This is from a book I read 7 years ago and still remember called The Index Card.

Here are my 3 favorite rules:

Rule #3: Max out your 401K and other tax-advantaged accounts.

Free money from your employer. Take it. If your company matches 3%, contribute at least 3%. That’s an immediate 100% return on your investment.

Beyond the match, you’re getting tax benefits — either upfront (traditional 401K) or in retirement (Roth).

Rule #4: Never buy or sell individual stocks.

You’re not smarter than the market. Neither am I. Sorry, Dad. (We’ve had this debate many times.)

Research shows almost nobody beats the market long-term by picking stocks.

Same goes for if you have a lot of one stock right now. Slowly sell this over time in regular intervals / amounts. The fancy name for this is reverse dollar-cost averaging.

Holding too much of something because you’ve had it for a long time (i.e. Google, ahem, guilty!) is the same as buying an individual stock.

Rule #5: Buy inexpensive, well-diversified index funds.

Set it and forget it. Boring beats exciting when it comes to investing. An index fund is like owning a tiny slice of the entire market. If the market grows, you grow with it.

The market (using the S&P 500 as a proxy) has returned 11.94% over the last 50 years, or 8.02% adjusted for inflation. I’ll take that return all day long.

When someone tries to sell you complicated financial products, come back to these basics.

I’ve followed these rules for my entire career, and they’ve served me well.

From my first Google paycheck to leaving to start my own business, these fundamentals never change.

Want more? Subscribe to my newsletter!

How This Helps You Get What You Want

You don’t need an MBA or a finance background to build wealth.

You just need to:

- Save consistently (10–20% if you can)

- Max out your 401K and take advantage of employer matching

- Never buy or sell individual stocks

- Invest in low-cost, diversified index funds

Everything else? Optional.

So instead of obsessing over that 200-page personal finance book you never finished, pick one or two rules from this card and practice them this month.

Complexity is the enemy of execution.

Keep it simple. Keep it consistent.

OTHER POPULAR ARTICLES

For more actionable tips to thrive professionally and personally, sign up for Jenny's newsletter.

Embrace the 9 traits of wild courage. Achieve your biggest ambitions.

order now

Weird

Selfish

Shameless

Obsessed

Nosy

Manipulative

Reckless

Brutal

Bossy

Weird

Selfish

Shameless

Obsessed

Nosy

Manipulative

Reckless

Brutal

Bossy

A rebellion against conventional

career wisdom, from

a former Google executive who spent 18 years climbing

the ranks

order now